Short-term business loans are designed for companies in need of quick cash so you can capitalize on a growth opportunity or manage unforeseen expenses. In contrast with other types of term loans, short-term loans normally come as a lump sum or a line of credit that is expected to be repaid within a year.

These loans offer a range of benefits, including faster approval processes, shorter repayment periods, and fewer qualification requirements compared to traditional long-term loans. Whether you’re looking to manage cash flow gaps, purchase inventory, or fund a marketing campaign, a short-term business loan can help.

To find the best short-term business loans, we did extensive research on 26 top nationwide lenders, analyzing contracts, interest rates, loan amounts, and qualifying requirements. To narrow the field, we also considered customer reviews as well as other expert opinions to help you to determine which is the best solution for your business.

Best Short-Term Business Loans

| Lender | Loan Amounts | Term Length | Credit Score |

|---|---|---|---|

| National Business Capital | $10,000 to $10 million | 6 to 36 months | 580 |

| Fora Financial | $5,000 to $1.5 million | up to 15 months | 500 |

| Bluevine | $6,000 to $250,000 | 6 to 12 months | 625 |

| Kapitus | $10,000 to $500,000 | 4 to 18 months | 630 |

| Amex Business Line of Credit | $2,000 to $250,000 | 6 to 24 months | 660 |

| OnDeck | $5,000 to $250,000 | 12 to 24 months | 625 |

| QuickBridge | $10,000 to $500,000 | 4 to 18 months | 650 |

1. National Business Capital

Best for businesses seeking varied loan options and personal guidance through the lending process with its marketplace of 75+ lenders

National Business Capital offers a wide variety of short-term loans for business owners. They excel at having a fast, online application process that lets you look at loans from multiple lenders without getting inundated with . As long as you meet the revenue requirement to qualify for a loan, NBC is a great partner to work with.

To get a short-term business loan with National Business Capital, your company must be in business for at least a year. If you are approved for multiple loan types, you can potentially get funding up to $10 million. Depending on the loan amount, it’s possible to get the funds in your bank account within just a few hours.

Interest Rates & Fees

National Business Capital provides short-term loans between $10,000 and $10 million. Depending on your creditworthiness and the loan type, the interest rate can range between 5 and 60%. Term lengths vary between 6 to 36 months. National Business Capital uses multiple lenders, but the typical interest rate for a term loan is 9.25% for loans from banks. For non-bank loans, you’ll generally pay 1% of your principal per month.

There are no upfront fees, but factor rates can multiply the entire loan by 1.1 or more. Factor rates can change between different loan products, so carefully read through the fine print before signing any agreements.

Eligibility Requirements

To quality for a loan through National Business Capital, your business must earn at least $480,000 per year. Ideally, this lender prefers companies that have a 680 credit score or higher, but they will work with you if your business has been in operation for a long time.

Unlike some lending institutions, National Business Capital lets you get short-term loans with bad credit, good credit, and everything in between. You will generally need a 580 for term loans, 600 for lines of credit, and 685 for loans from the SBA.

Products Offered

National Business Capital will help you find and compare loans from many different lenders and loan programs. For example, you can work with National Business Capital to get Small Business Administration (SBA) loans. This organization offers the following financial products.

- Asset-based lending

- Business term loans

- SBA loans

- Subordinated debt

- Small business loans

- Revenue-based financing

- Equipment financing

- Business line of credit

Application Process

Unlike some financial institutions, you don’t have to show your tax returns to get a loan. You will need to create an online account to access National Business Capital’s lenders. The online application takes just a few minutes to complete. Afterward, you can immediately see which lenders and loan programs you qualify for.

Customer Support Access & Hours

Customer support can be reached at (888) 488-4769 or online. National Business Capital is open 24 hours a day, so you can access customer support whenever you need it.

National BUsiness Capital Pros & Cons

| Pros | Cons |

|---|---|

| • No upfront fees | • Requires revenue of $40k+ month |

| • Bad credit options available | • Must create an account to apply |

| • Tax returns aren't required | |

| • Over 90% of applicants get approved |

2. Fora Financial

For merchants looking for straightforward short-term funding with early payment discounts but without strict credit score requirements

If you want to quickly get short-term loans online, check out Fora Financial. This organization has helped small businesses access the funding they need for over a decade. Fora has provided more than 55,000 companies with over $4 billion in total funding.

Fora Financial truly excels when it comes to the amount you can borrow. While some financial institutions will not loan low amounts, Fora will give you a short-term loan for just $5,000. On the higher end of the scale, you can borrow up to $1.5 million.

Overview

If you have bad credit, Fora Financial is one of the best short-term business loans available. Plus, your business only has to be in operation for three months. Once you meet the minimum qualifications, you can quickly apply for your loan and get it funded in 72 hours or less.

Interest Rates & Fees

The biggest frustration involved in working with Fora Financial is figuring out the fee and interest rate structure. Until you have applied and been approved, you won’t get to see your short-term business loan’s interest rate or fees. You can expect to pay an origination fee of at least 3% and factor rates between 1.1 and 1.9.

Eligibility Requirements

With Fora Financial, you can find short-term loans for business owners who only have a 500 credit score. You must earn a minimum annual revenue of $144,000. Unlike most short-term loans online, you just have to be in business for three months to qualify.

Products Offered

Fora Financial offers short-term loans and merchant cash advances to qualified businesses.

- Short-term loans: These loans are available with factor rates between 1.1 and 1.9. You can get them for any amount between $5,000 and $1.5 million. The maximum term length is 16 months.

- Merchant cash advances: A merchant cash advance is also known as a revenue advance. Basically, it involves borrowing money and then paying it back through your earnings. For this type of financing, you can expect to pay between 0 to 24.99% interest.

Application Process

You can fill out an easy application online. Initially, you will need to provide three months of your company’s bank statements, but you may also need to give Fora Financial your tax returns, bank statement, balance sheet, annual revenue, or profit and loss statement.

Afterward, an application specialist will give you a call to talk about your application. They will need to get a voided check, a copy of your driver’s license, and proof of your business ownership before they can approve your loan. Once you are approved for short-term business loans through Fora Financial, you can expect funding within 24 to 72 hours.

Customer Support Access & Hours

For customer support, call (877) 419-3568 from 9 AM to 7 PM. You can also email them at customerservice@forafinancial.com.

Pros & Cons of Fora Financial

| Pros | Cons |

|---|---|

| • Low borrowing minimum of just $5,000 | • High interest rates |

| • No collateral required for most loans | • Won't provide total costs upfront |

| • Use loan money for any business purpose | |

| • Accepts businesses with lower credit scores |

3. Bluevine

Best for small businesses looking for fast approval and funding with a flexible line of credit for short-term cash flow needs

Bluevine is a fintech company that provides online banking and financing services, specifically geared towards small business owners. They aim to simplify banking by offering a user-friendly experience and quick access to loans and lines of credit, compared to traditional banks.

Bluevine’s short-term business loans are designed to help entrepreneurs meet immediate funding needs, such as covering payroll, inventory purchases, emergency repairs, or taking advantage of time-sensitive business opportunities.

Bluevine Interest Rates & Fees

The Bluevine Business Line of Credit has an interest rate of 7.8% for well qualified borrowers. There are no prepayment penalties or monthly maintenance fees, but late fees may apply. If you want to receive funds through a wire transfer, you will have to pay a $15 fee.

Requirements

While a short-term loan requires a 650 credit score, lines of credit can be accessed with just a 625 credit score. Depending on the type of short-term financing you want, your business will need to earn a minimum of $100,000 to $480,000 per year. You will need to provide basic information about your business, such as your bank statements from the last three months. Additionally, your company must be in good standing.

Loans Offered

Bluevine offers short-term loans and a business line of credit. Each comes with its own benefits and drawbacks.

- Short-term loans: These are available with up to two-year repayment terms. Your business must earn $100,000 to $150,000 in annual revenue to qualify. In addition, you must have a 650 credit score and two years of business history.

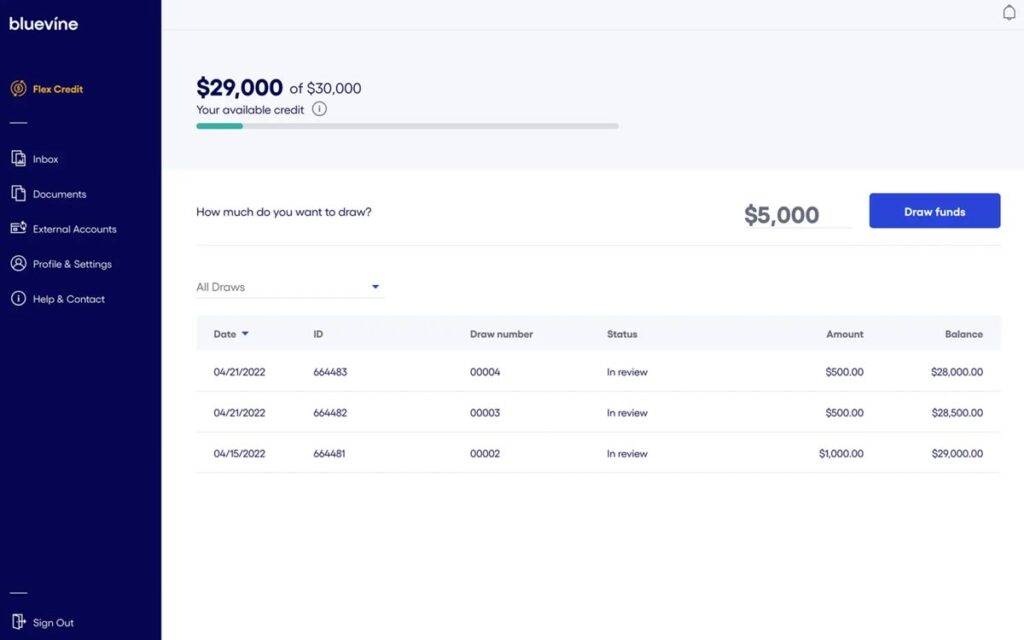

- Lines of credit: You can get lines of credit for up to $250,000. After applying online, you can get access to your funds in just a few hours. To qualify, your business must earn $40,000 in revenue each month and have a two-year history. Additionally, you need a 625 credit score or higher.

Application & Funding

The Bluevine application process can be completed in about five minutes. It’s really easy, especially because they have an option to connect to your QuickBooks account.

To apply, you’ll set up an online account. You will need to submit the last three months of your company’s bank statements and basic business information.

The initial application does a soft pull on your credit, so it won’t affect your credit score. Once approved, you can often access the funds within a few hours.

Bluevine Summary

| Loan Amounts | Up to $500,000 |

| Minimum Credit Score | 625 |

| Estimated APR Range | 7.8% to 43% |

| Revenue Requirement | $40,000 in monthly revenue |

| Underwriting Process | Connect bank accounts & QuickBooks |

| Credit Check | Soft Pull |

| Approval Time | 5 minutes |

| Collateral Required | Personal guarantee |

If you have an established corporation or LLC with a fair credit score and need quick access to short-term financing, Bluevine could be a good fit. However, if your business is newer, has lower revenue, or is not structured as a corporation or LLC, you may want to explore other options.

4. Kapitus

Best for businesses seeking flexible short-term loans geared towards quick expansion or inventory purchase

Since its founding in 2006, Kapitus has provided over $5 billion in capital to more than 50,000 businesses in the US. With their fast short-term business loans, you can finish an application in just five minutes or less. Plus, you have financing options beyond basic short-term loans. If you want invoice factoring, SBA loans, or business lines of credit, Kapitus has you covered.

Kapitus Overview

Short-term business loans from Kapitus have monthly, weekly, biweekly, and daily repayment options. You can also choose to have a loan term as long as five years and as short as three months.

Because many of the loan fees and rates aren’t disclosed on their website, you should take time to read through the loan offer before you agree to it.

Kapitus has a wide array of short-term loans for business owners, so they are a good place to go if you need help funding your day-to-day operations or dealing with emergency situations.

RELATED: Full Review of Kapitus Revenue-Based Financing

Interest Rates & Fees

Kapitus offers a variety of loan types and the rates vary depending on the duration. For purchase order financing, you can get a factor rate of 1.25. Meanwhile, the Kapitus+ line of credit has an origination fee of 2.5% to 3% and an interest rate of 1-5% per month.

Eligibility Requirements

To get a short-term loan from Kapitus, you must have a 630 credit score. In addition to being in business for at least two years, your organization must earn a minimum of $250,000 in average annual revenue. If you have excellent credit, you may qualify for one of their loans with just one year of business history.

Products Offered

Where Kapitus really excels is with its range of financial products. Each one has different eligibility requirements, so it’s important to talk to a loan specialist after you complete your application.

- Small business loans

- Equipment financing

- Business line of credit

- Merchant cash advance

- Revenue-based financing

- SBA loans

- Invoice factoring

- Purchase order financing

Application Process

You can complete your loan application in as little as five minutes. If everything is in order, you can get your application approved in just four hours.

Customer Support Access & Hours

For help with your loan, you can contact Kapitus by phone or email. Their phone line can be reached at (800) 780-7133 between 9 AM and 6 PM on Mondays to Fridays. If you are trying to reach them outside of normal business hours, you can also get in touch using their email form.

Pros & Cons of Kapitus

| Pros | Cons |

|---|---|

| • Fast online application | • Requires revenue of $20k+ month |

| • Wide variety of financial products | • Fees aren't disclosed until after you apply |

| • Quick funding in 24 to 48 hours | |

| • Loan terms from 3 months to 5 years |

5. American Express Business Line of Credit

Ideal for American Express card members seeking a revolving line of credit with competitive rates and no collateral requirement

A line of credit is like a flexible loan from a bank. Like a credit card, it allows you to increase or decrease the amount you borrow as you need to. With Amex Business Line of Credit, you can get instant access to funds whenever you need them.

Overview

Amex Business Line of Credit is great if you want an accessible financial option and an easy application process. It is not ideal if you’re searching for a low short-term business loan interest rate.

Fortunately, there is no prepayment penalty, so you can easily avoid some of the interest rate charges by paying off your line of credit early. For borrowers with a steady source of revenue and decent credit, this type of short-term financing is a good option.

Interest Rates & Fees

With the American Express Business Line of Credit, you don’t have to pay an application fee, origination fee, monthly maintenance cost, or annual fee. You will only be charged fees for late or unsuccessful payments. During your loan term, you can expect to pay the following monthly fees instead of a traditional interest rate.

- Six-month loans: 3 to 9%

- 12-month loans: 6 to 18%

- 18-month loans: 9 to 27%

- 24-month loans: 12 to 18%

Eligibility Requirements

To apply for Amex Business Line of Credit, you must be at least 18 years old. Your business must have started at least one year ago. Additionally, you need a FICO score of 660 and $3,000 in average revenue per month.

Products Offered

Amex Business Line of Credit is available for amounts ranging between $2,000 and $250,000. You can qualify for six-month, 12-month, 18-month, or 24-month loan terms.

It is really important to understand how this kind of line of credit is set up because it is a little different than a traditional loan or credit card. Each time you pull money from your line of credit, the transaction is given the interest rate and payoff timeline for your line of credit’s loan term.

Let’s assume that you have an Amex Business Line of Credit with a 12-month term. Today, you decided to borrow $10,000 from your line of credit. Now, you will repay that $10,000 over the next 12 months. Each month, Amex will also charge you 6 to 18% of the $10,000 principal. If you borrow anything else, the new transaction will be given its own 12-month term.

Application Process

The application process is completely automated and online. You can apply and get approved in minutes for short-term business loans. To apply, you will need to provide your business tax ID (EIN), your company’s industry, your Social Security number, and your estimated annual gross revenue.

Customer Support Access & Hours

You can easily reach American Express through online chat or via phone. To talk about your line of credit, call customer service at 1-888-986-8263. They are available on Mondays to Fridays from 8 AM to 9 PM EST and Saturdays from 10 AM to 6 PM.

Amex Business Pros & Cons

| Pros | Cons |

|---|---|

| • Streamlined application | • Requires a personal guarantee |

| • Accessible for businesses with fair credit | • Only offers a line of credit |

| • No hidden fees | • Monthly fees can add up quickly |

| • Ideal for shorter term lengths |

6. OnDeck

For business owners in need of same-day funding who are willing to pay higher rates for quick, unsecured short-term loans

When you apply for short-term loans with OnDeck, you can enjoy having fast funding options. If your application is in order, you can even get same-day funding. Additionally, loan terms are available for up to 24 months.

Overview

If you need short-term loans with bad credit or fair credit, OnDeck has a few options you can choose from. While they charge a higher interest rate than some lenders, OnDeck truly excels when it comes to providing same-day funding. This is the best option for business owners who need fast funding for large loans and lines of credit.

Interest Rates & Fees

If you’re considering short-term business loan interest rates, OnDeck might not be the best choice. OnDeck charges factor rates, which are between 1.037 and 1.45 for term loans. For lines of credit, they are between 1.10 and 1.30. This works out to an APR of 35.5 to 99.9% for term loans and 39.9 to 77.9% for lines of credit.

With a term loan, you also have an origination fee between 0 and 4%. Meanwhile, you’ll have to pay a $20 maintenance fee each month for a line of credit. If you pull $5,000 or more in the first week after you open your line of credit, the maintenance fee will be waived for six months.

Eligibility Requirements

To get small business loans for startups and established companies, you must have a 625 credit score or higher. OnDeck requires companies to have at least a 12-month history of operations and a business checking account. Additionally, your business must earn $100,000 or more in annual revenue.

Products Offered

There are two basic short-term financing products at OnDeck. You can get a line of credit or a term loan. The type of financial vehicle you choose can vary based on your credit score, repayment needs, and the amount you want to borrow.

- OnDeck Line of Credit: This line of credit can be funded in seconds for credit limits ranging between $6,000 and $100,000. You can select 12-month, 18-month, or 24-month repayment terms.

- OnDeck Term Loan: These short-term loans have repayment terms that can last for up to 24 months. They are given as a lump sum for amounts ranging between $5,000 and $250,000.

Application Process

Figuring out how to get a short-term loan with OnDeck is fairly straightforward. You must fill out the easy online application with basic information about your company. Additionally, you will need to provide basic documents, like your company’s recent bank statements. Afterward, a loan advisor will talk to you about the options you qualify for. Depending on how much you need, you may be able to access all of your funds on the same day that you turn in your application.

OnDeck Customer Support Access & Hours

After you apply for short-term loans for business owners, you may have questions or concerns. OnDesk can be reached at (888) 269-4246 on Mondays to Fridays between the hours of 9:30 AM to 7:30 PM EST. You can also email them at customerservice@ondeck.com for help with an existing loan.

Pros & Cons of OnDeck

| Pros | Cons |

|---|---|

| • Same-day funding | • High interest rates |

| • Check eligibility w/o hard credit pull | • Requires $100k+ annual revenue |

| • Flexible application requirements | |

| • Borrow up to $250,000 |

7. QuickBridge

Perfect for businesses seeking rapid, short-term funding solutions with personalized customer service and minimal paperwork

If you’re looking for the top short-term loans for business owners, QuickBridge is the place to go. You can qualify for short-term loans for business owners with just six months of business history. However, you will need to earn at least $250,000 in revenue each year. As long as you meet these requirements, QuickBridge may be able to help you meet your funding goals.

Overview

As one of the best short-term business loans, QuickBridge offers an incredibly fast application process. Best of all, you may be able to qualify for a discount if you pay off your loan early. If you need a working capital loan or emergency funding, this financial institution has multiple options available.

Interest Rates & Fees

At QuickBridge, you can expect to pay a 1.1 factor rate or higher. This works out to an APR that is above 20%. No matter what factor rate you pay, you will likely be charged an origination fee between 1 and 5%.

Eligibility Requirements

To be eligible, you must be in business for at least six months and have a credit score of 600 or higher. For basic business loans, you will need to earn at least $250,000 in annual revenue. Equipment financing may have different requirements.

Products Offered

At QuickBridge, you can find short-term and long-term business loans. In addition, you can access emergency loans and working capital loans when your company needs cash quickly.

- Working capital loans: Working capital loans can help you maintain your daily operations if your business is temporarily short on cash. They are intended to bridge a gap in cash flow and cover emergency expenses, so they have short repayment timelines.

- Short-term business loans: When you access QuickBridge’s short-term loans for business owners, you can enjoy having 4-month to 18-month repayment terms.

- Emergency loans: You can get emergency loans for unexpected problems, like a natural disaster or power outage. Emergency loans are available for up to $500,000 and take 24 hours or less to fund.

Application Process

To figure out how to get a short-term loan, start with their online application. You will need to provide some personal information and information about your business, like your gross sales. Then, you will need to provide a copy of your driver’s license and your company’s bank statements. QuickBridge will use that information and your credit score to decide if you qualify for a loan or not.

Customer Support Access & Hours

If you need help with your short-term business financing, you can call QuickBridge at (888) 233-9085 on Mondays to Fridays between 6:30 AM and 5 PM.

QuickBridge Pros & Cons

| Pros | Cons |

|---|---|

| • Flexible loan amounts | • Potential for high fees |

| • Fast approval and funding (within 24 hours) | • May require a personal guarantee |

| • Minimal paperwork required | |

| • Accepts businesses with lower credit scores |

How Short-Term Business Loans Work

What is a Short-Term Business Loan?

Short-term business loans are a type of alternative financing options designed to meet immediate financing needs of a business, typically requiring repayment within a year. These loans provide businesses with quick access to working capital for a variety of operational purposes.

Loan Maturity Terms

The term lengths for short-term loans can vary significantly, usually ranging from three months to one year, but may extend to 18 months or longer in some cases. The structured repayment schedule usually aligns with the company’s cash flow pattern.

Application Process

The application process for such loans is generally simpler and faster compared to long-term loans, often with online applications and limited documentation. Lenders may provide a decision rapidly, often allowing businesses to access funds in 24 hours or less.

Repayment Plans

Repayment terms for short-term loans are often set as fixed lump-sum payments at regular intervals (weekly, bi-weekly, or monthly). Some lenders might link repayment to the business’s daily sales or receivables for flexibility.

Types of Short-Term Loans Available

There are various types of short-term loans, including traditional bank loans, lines of credit, merchant cash advances (MCAs), invoice financing, and more unconventional platforms like peer-to-peer lending—all catering to different short-term financial needs.

Short-Term Loan Interest Rates

Typically, short-term loans have higher annual percentage rates (APRs) than long-term loans due to the lenders’ need to make a profit within a shorter timeframe and to offset the increased risk associated with faster lending decisions and less stringent borrowing requirements.

Currently, short-term business loan interest rates typically range from 6% to 36% APR, with an average around 13-16% for traditional bank loans. Online lenders may offer rates starting as low as 7% for highly qualified borrowers, but can go up to 100% or more for high-risk applicants.

The interest rates on short-term business loans can be influenced by several factors:

- Creditworthiness of the borrower and the business

- Annual revenue of the business

- Loan amount

- Debt service coverage ratio (DSCR)

- Lender policies

- Macro market conditions

The range of interest rates can be broad, often stretching from single-digit percentages for lower risk scenarios up to much higher rates for loans perceived as high-risk or for products like merchant cash advances. The specific rate a business will receive depends largely on its creditworthiness and market conditions.

How to Get a Short-Term Business Loan

To be eligible for a short-term business loan, borrowers typically need to meet certain criteria set by the lender, such as a minimum credit score, a specified amount of time in business (usually at least one year), and minimum annual revenue requirements. A solid business plan and a clear purpose for the loan can also play a significant role in eligibility.

Applying for a short-term business loan usually involves providing documentation that may include business financial statements (like profit and loss statements, balance sheets, and cash flow statements), tax returns, a business plan, bank statements, and sometimes accounts receivable and payable aging reports.

Application Process

- Research potential lenders to find the best terms and rates.

- Prepare the needed documentation and information regarding your business’s financial status.

- Submit the application either online or in person, depending on the lender’s process.

- Wait for the approval process, which may involve additional questions from the lender or requests for more documentation.

- Review any offers carefully including terms, interest rates, fees, and repayment schedule.

- Sign the agreement if you find that the loan meets your needs.

Advantages of Short-Term Business Loans

- Accelerated Funding: These loans are usually processed quickly, providing businesses with timely financial support for urgent needs.

- Flexibility: Multiple product types and lending terms offer a wide range of financing options based on the specific needs of different businesses.

- Streamlined Application Process: The paperwork and approval process for short-term loans are often less complex than those for long-term loans.

- Easier Approval: Lenders may have less stringent criteria, benefiting smaller businesses or those that don’t qualify for traditional bank loans.

- No Long-Term Commitments: Businesses can manage debts without long-term financial obligations, possibly minimizing total interest paid over time.

Risks of Short-Term Business Loans

- Higher Cost of Capital: The annual percentage rates and interest costs are generally higher compared to long-term options, meaning you’ll pay more over time.

- Frequent Repayments: Often these loans require frequent repayments which can strain a business’s daily or weekly cash flow.

- Risk of Debt Cycle: Continuous or repeated reliance on short-term credit could kickstart a cycle of debt that’s hard to break from.

- Potential for Higher Rates with Poor Credit: Businesses with less than ideal credit may still obtain loans, but likely at an increased rate, elevating financial expense burdens.

- Limited Borrowing Amounts: Typically, short-term loans offer lower capital amounts than longer-term loans, possibly insufficient for substantial investment opportunities.

Are Short-Term Business Loans the Solution?

Short-term business loans are a solution for companies that need cash fast. While they can help increase working capital, bridge revenue gaps, cover unexpected costs, or allow you to pursue growth opportunities, they also have high interest rates and frequent payments, posing potential risks.

Before taking out any loan, ensure your business is financially stable and that you fully understand the loan terms. It’s crucial to be realistic about repaying without hurting cash flow. Use short-term loans strategically—they need to benefit your business in the long run.