Restaurant bookkeeping is vital for business health. We all know that successful restaurant owners keep an eye on their finances as much as getting food in front of customers.

If you place a value on your time of at least $30 an hour, it’s worth it to work with a bookkeeping service. Sure, you can get by using QuickBooks or free bookkeeping software, but you’re likely to spend three to four hours on it each month (and many more during tax season). Restaurant bookkeeping services can do a better job and the best services add value to your business.

This guide covers everything you need to know about restaurant bookkeeping. It starts with the best bookkeeping services that allow you to concentrate on running your restaurant. Then, we’ll get into restaurant-specific expense tracking, key performance indicators (KPIs), analysis, and financial reporting.

Best Bookkeeping Services for Restaurants

To determine the best services, we reviewed dozens of services looking for those with an excellent reputation that also specialize in restaurant bookkeeping.

| Bookkeeping Service | Best because |

|---|---|

| Bookkeeper360 | Can also help with accounting, HR, and payroll |

| Xendoo | Customized bookkeeping |

| Reconciled | Responsive and engaged bookkeepers |

| Streamline Bookkeeping | Excellent value |

1. Bookkeeper360

Bookkeeper360 is a full-service back office accounting solution. You’ll get financial reports including a P&L, customizable goals, and year-over-year metric comparisons without having to use spreadsheets.

Bookkeeper360 is one of the simplest to use and makes monitoring cash flow and payroll a breeze. You can also access a team of certified accountants on an as-needed basis with Bookkeeper360.

| Bookkeeper360 Service | Features | Pricing From |

|---|---|---|

| Bookkeeping | Cash or accrual bookkeeping, monthly or weekly reconciliation | $399/mo |

| Controller | Bookkeeping, advanced reporting, annual budget, KPIs | $1,149/mo |

| Catch-up Bookkeeping | Create & restructure chart of accounts | $1,000 |

| Tax | Business & individual taxes | $350 |

| Payroll Administration | Time tracking, payroll processing | $200/mo |

| Sales Tax | Monthly or quarterly filing, state registrations, nexus studies | $125/mo |

| Back-Office | AR / AP, inventory management, expense management | $150/mo |

| CFO Advisory | Projections, forecasts, financial plans, strategic growth & vision | $1,500/mo |

2. Xendoo

Xendoo offers customized bookkeeping and financial help for restaurants. With pricing starting at only $395 per month, they are also one of the more affordable virtual bookkeeping services.

If you’re looking to simplify your back office with a single partner, Xendoo is a great option since their dedicated US-based team can handle your bookkeeping, accounting, tax prep, and payroll. If you want a service you can customize, Xendoo is also a great option.

| Xendoo Plan | Features | Number of Accounts | Average Monthly Expenses | Cost |

|---|---|---|---|---|

| Essential | Weekly bookkeeping, Dedicated team | Up to 4 | Up to $50k | $395 per month |

| Growth | Cash or modified accrual, Tax consult | Up to 6 | $50k to $75k | $695 per month |

| Scale | Custom chart of accounts, Deferred schedules | Up to 12 | $75k to $125k | $995 per month |

3. Reconciled

Reconciled is one of the best online bookkeeping companies because it is a one-stop shop for restaurant accounting. Best of all, you get responsive and engaged bookkeepers working on your reports and documents.

Whether it’s monthly reports or filing your taxes, Reconciled is a great way to make sure you’re on the right side of relevant regulations and on the path to profitability.

As a new client, Reconciled will bring in an expert from their implementation team to analyze your books. They also create processes that detail exactly how you want your bookkeeping completed. This helps your bookkeeping team ensure accuracy and consistency.

| Reconciled Plan | Features | Monthly Price |

|---|---|---|

| Express | 3 accounts, less than $1M revenue | Starting at $475 |

| Basic | AP support, 5 accounts | Starting at $625 |

| Core | Monthly Meetings, 7 accounts | Starting at $775 |

| Advanced | AP / AR support, 7 accounts | Starting at $925 |

4. Streamline Bookkeeping

Streamline Bookkeeping is really helpful when it comes to protecting restaurant owners against fraud. The forms they produce are tax-ready, which will make filing easier when the time comes. Streamline is one of the most affordable bookkeeping services with an all U.S. staff.

What stands out most about Streamline Bookkeeping is that each client gets a dedicated a three-person team led by a CPA reviewing your file. They also use read-only access to your financial institutions and they’re really into working in a way that satisfies each individual client.

| Streamline Bookkeeping Plan | Average Monthly Transactions | Monthly Price |

|---|---|---|

| Small Business | Up to 60 | $199 |

| Custom | More than 60 | Custom |

Related: Best Virtual Bookkeeping Services

Restaurant Bookkeeping Metrics

We interviewed successful restaurateurs and found they rely on these metrics to benchmark performance and inform their decision-making.

Cost of Goods Sold (COGS)

A simple measurement of the value of the goods you need to make your dishes is the cost of goods sold. Cost of Goods Sold (COGS) is the direct cost to produce the service or product that you are providing.

To calculate the COGS, subtract the ending inventory from the sum of your beginning inventory and any supplies you bought after the initial inventory.

COGS Formula

Initial Inventory + Purchases – Ending Inventory = Cost of Goods Sold

Sometimes, you just want to look at how much your necessary ingredients cost. Make sure to include everything you buy, from the spices to small garnishes and sauces. It’s simple, but COGS forms the foundation of most other calculations.

Food Cost Percentage (FCP)

Your food cost percentage – that is, what percentage of your sales are spent to make a dish – helps you calculate what dishes are profitable.

Since FCP takes your inventory into account, it can work as an alert when problems arise. If your FCP starts to shoot up then you’re either wasting food or spending too much on ingredients.

FCP Formula

(Beginning Inventory + Purchases – Ending Inventory) / Food Sales = FCP

While there is no perfect food cost percentage, the owners we interviewed for this guide agree that FCP under 30 percent is considered good. Most restaurants try to keep their FCP under 35 percent.

Benchmark Using Income Based KPIs

Now that you know how to analyze your expenses, there are two indicators of value worth tracking.

Sales per Square Foot

Sales per Square Foot will help you monitor the efficiency and value of your total real estate space available to you. It may even help if you are able to make additional accommodations within the space available, such as adjusting the seating to be flexible to smaller groups as well as larger groups.

Sales per Square Foot = Sales / Total Square Foot

Revenue per Seat

Revenue per Seat is the total amount of revenue divided by the number of seats available on any given night. The point is to understand the value per seat, with low numbers being less desirable since they would indicate an issue with pricing or slow business.

Revenue per Seat = Revenue / # Seats Available

Restaurant Expenses

Most restaurants share similar expenses, and we’ve talked about the two major ones being COGS and labor. There is another way to look at expenses that has a holistic view of the entire company by breaking them down into four categories: Fixed, Variable, Mixed Use, and Sunk Cost.

Fixed Cost

Fixed costs don’t change over time. Fixed restaurant costs include rent or mortgage, licenses, insurance, and support services such as accounting and marketing. When reviewing your financials or budgeting, these costs will not change and must be covered by sales every month.

Variable Cost

Variable cost may increase or decrease seasonally or based on demand. These are usually things like food costs and repairs. While food costs are the most obvious, and repairs are due to the additional wear and tear from the patrons and staff.

Mixed Use Cost

Mixed use costs are usually fixed but may vary. For example, utility use may rise above average during hot weather when more water and beverages are consumed. The biggest mixed use cost is labor, especially for businesses that have highly cyclical demand such as seasonally affected tourist areas.

Sunk Cost

Sunk costs are those that have occurred and you cannot recover. These are not ongoing, and may be “the cost of doing business.” The biggest sunk cost for restaurants is the kitchen equipment. Loans are often taken out for this purpose alone.

Familiarizing yourself with these four categories will help in decision making. While there isn’t an industry specific ratio to track each of these expenses, it’s best to review every month.

Financial Reports for Restaurant Owners

Bookkeeping reports offer insights about the health and profitability of your restaurant. Here are some financial reports you should run regularly to get the information you need:

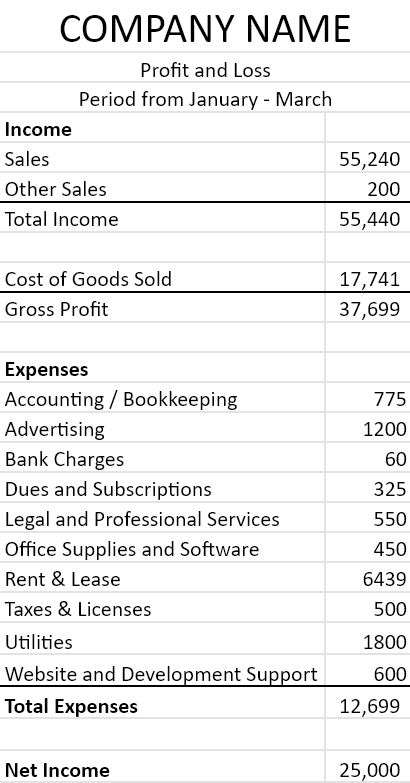

Profit & Loss Statement (P&L)

The Profit & Loss statement is the hallmark of business reports. Your P&L should show the information about food costs, expenses, and sales. It can also compare the current period to the same time period from the previous year to help you see trends and fluctuations.

A well constructed Profit and Loss statement will start by showing the total income at the top of the report. Then it will subtract COGS, and the remaining number is gross profit.

The next section of the profit and loss will detail all of the expenses by category and end with a total expense number. The last section takes your gross profit and subtracts your expenses to show your net profit (or loss).

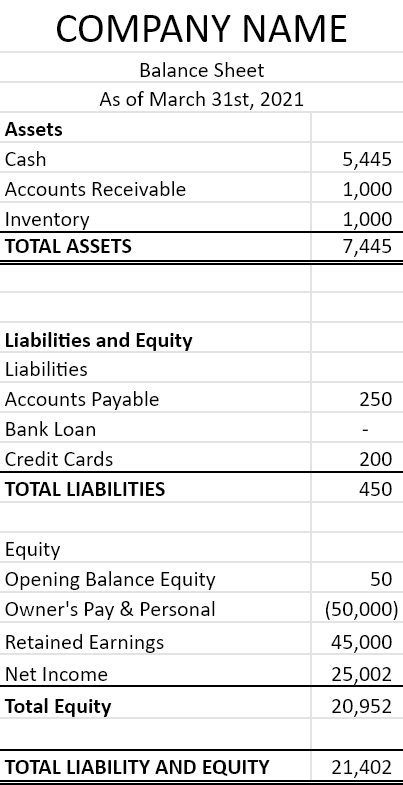

Balance Sheet

The balance sheet shows all of the assets, liabilities, and capital that a business has at a specific point in time. Essentially, the balance sheet shows what a business owns and what it owes.

Assets are items of value (cash, inventory, property, equipment, etc.).

Liabilities are things that are owed (loans, accounts payable, open balances with other vendors, etc.).

POS Systems and Daily Sales Report

Point of Sale systems handle your basic check out and payment, but the right system for you may include many more features. It may even help answer questions such as what is your most popular dish, peak volume periods, and if you need to expand store hours.

You can then apply that to understanding what inventory you need to purchase more of, which dishes to feature or discontinue, and when to ensure you have additional staffing.

Related: Everything About Point of Sale

With a POS system, everything sold during the day is categorized on the daily sales report. X-reports and Z-reports have a similar function to track sales and refunds. Make sure your POS system creates the daily sales report in an easy to read format that’s printable.

Reviewing a daily sales report may help you catch fraud. You may see the drawer a little over and under, but when there’s a pattern or a specific number (i.e. exactly $20 every Thursday) it may be telling you something else.

Restaurant Budgeting and Forecasting

Budgeting is used to manage financial constraints – anticipated operational expenses and revenue.

There are a variety of ways to create a budget or a forecast, and many accounting systems offer some level of budgeting. See below for an example of actual and forecasted financials.

| Actual | Forecasted | |

|---|---|---|

| Sales | 8,000 | 12,000 |

| Expenses | ||

| Cost of Goods Sold | 3,500 | 5,000 |

| Accounting | 325 | 450 |

| Legal | 0 | 150 |

| Marketing | 275 | 400 |

| Profit | 3,900 | 6,000 |

Forecasting is forward looking, focusing on a reasonable goal (i.e. increased COGS for an anticipated revenue increase to due a reasonably estimated demand).

Forecasting basics to help you get started:

- Expectations: Define the time period you’re budgeting for and document your expectations.

- Seasonal sales increase/decrease, staffing adjustments, and inventory pricing changes.

- Expenses: Use your P&L report and review the previous period for expenses.

- Review the prior period or the same period from the previous year.

- Understand the factors influencing variable and mixed expenses.

- Consider upcoming one time expenses (sunk expenses).

- Revenue: Focus on revenue on your P&L.

- Review the income for the anticipated changes.

Always consider the cyclical nature of your business, where it is due to a seasonal influx of patrons or a shift in staffing due to the general age range employed.

Building a Profitable Menu

All the passion and care in the world won’t guarantee that a delicious dish will be profitable. The reality of the restaurant business is that your food has to bring in money or the doors will close.

Menu engineering can help ensure your restaurant stays in the black. Menu engineering incorporates the metrics we’ve discussed as well as a few others, particularly contribution margin.

Contribution Margin Formula

Cost of Dish – Sales Price = Contribution Margin

Fixed costs like rent and utilities are not included in this calculation, only the cost of ingredients. Think of contribution margin as profit available to settle fixed costs.

You can also work out the contribution margin of your entire menu and then stack the contribution margins of individual dishes against that number to make sure everything is in sync. When you introduce a new dish, you can set its price using the contribution margin and FCP to price it effectively.

In an ideal world, your contribution margin would be increasing over time while the food cost percentage decreases.

The contribution margin is a good indicator for a dish that has a high FCP, but is still profitable.

Last Call on Restaurant Bookkeeping

Restaurant bookkeeping helps you understand how metrics and reports can be used to assess the health of your business and come up with long-term strategies for profit and growth.

The bookkeeping services mentioned in this guide simplify things and let you focus on running your business. As with all our articles, we hope you learned something that will help your business.